Related Post

Feb 09, 2024

539 views

Challenges faced by VC’s to find the right startup for investment

Category: Blog

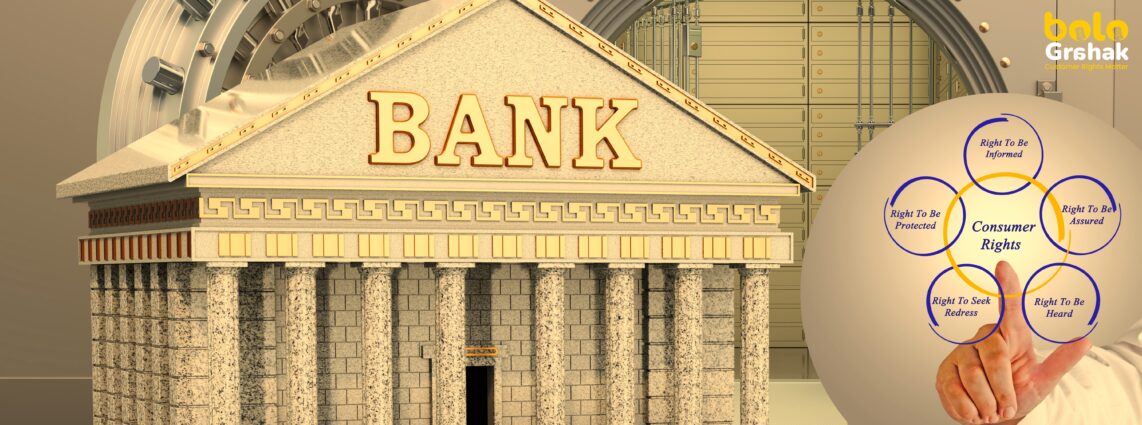

Consumer rights play a crucial role in maintaining trust and integrity in the banking sector. Banking fraud and mis-selling practices can have a devastating impact on individuals’ financial well-being. In recent years instances of fraud and mis-selling have surfaced leading to financial losses and consumer distrust. This blog will delve into the importance of consumer rights in banking, explore the consequences of fraud and mis-selling and discuss measures to address and prevent such practices.

The Significance of Consumer Rights in Banking: Consumer rights act as a shield against unethical practices ensuring fairness transparency and accountability in banking transactions. They empower individuals to make informed decisions protect their interests and seek recourse if they have been subjected to fraud or mis-selling. Banks have a fiduciary responsibility to act in the best interests of their customers which can be reinforced through strong consumer rights provisions.

Fraud in Banking: Banking fraud is a pervasive threat that spans from credit card fraud and identity theft to more complex schemes targeting personal and business accounts. It can result in significant financial losses damage to credit scores and a loss of trust in financial institutions. Common types of banking fraud include phishing scams counterfeit checks and fraudulent online transactions. To combat this issue banks must invest in robust security measures educate customers about potential risks and promptly investigate and resolve reported incidents.

Mis-selling in Banking: Mis-selling occurs when banks or financial institutions sell products or services to consumers that are not suitable for their needs or are misrepresented. Mis-selling is a common complaint in the banking industry. This unethical practice can lead to financial losses debt and erosion of trust. Examples of mis-selling include pushing unnecessary insurance policies misleading customers about the terms and conditions of loans or credit cards and selling complex financial products without proper explanation. This is a huge disservice to consumers as they may be investing in products that may not be as useful to them. To address mis-selling regulatory bodies need to enforce stringent rules and ensure that banks prioritise customers’ best interests.

Addressing Fraud and Mis-selling: To effectively address fraud and mis-selling in the banking sector several measures can be taken:

Protecting consumer rights and tackling fraud and mis-selling practices in the banking sector are paramount for ensuring a fair and trustworthy financial system. Strong regulatory frameworks consumer education proactive fraud prevention measures ethical sales practices and efficient complaint handling processes are essential to safeguard consumer interests. By addressing these issues effectively, we can build a more secure and accountable banking industry that serves the best interests of consumers.

Category: Blog

Your Comment